Calculate Your Paycheck in 7 Steps!

With a gross income of $1000, the net salary would be $723.50 after all deductions.

In this article we will take a detailed look at every component that contributes to your final take-home pay. There will be special attention to what makes Colorado unique, like not having state income tax, which impacts how your paycheck looks.

TABLE OF CONTENTS

Paycheck Calculator: What is My Gross Income?

It is the total amount of money you earn before taxes and deductions are taken. Depending on the context, it includes your basic salary or wages as well as any additional income sources you may have, like bonuses, overtime pay, commissions, and potential interest, dividend, and rental income.

In the specific context of calculating your paycheck:

For Salaried Employees: Your gross income is your annual salary. For instance, if you have a job that pays $50,000 per year, your gross income is $50,000.

For Hourly Employees: Your gross income is calculated by multiplying your hourly wage by the number of hours worked. For example, if you make $20 per hour and work 40 hours per week, your weekly gross income would be $800 (which is $20 x 40).

Additional Earnings: If you receive bonuses, commissions, or overtime pay, these are added to your regular pay to constitute your gross income.

Paycheck Calculator: What is My Federal Income Tax in Colorado?

Federal income tax is a tax imposed by the United States government on individuals, corporations, trusts, and other legal entities. This tax is applied to all forms of income that make up a taxpayer’s taxable income. This includes wages, salaries, commissions, bonuses, and any income from investments or business activities.

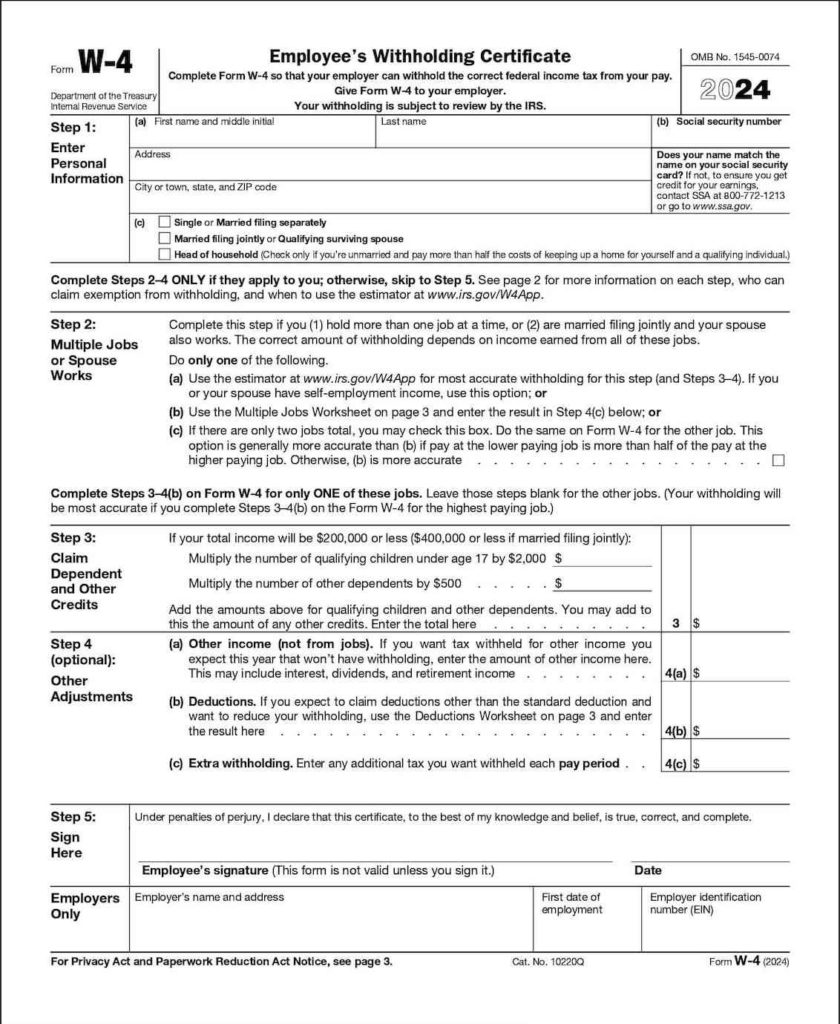

For your company to know your federal income tax, you will need to fill out the Form W-4, here’s why:

- Purpose of Form W-4: Form W-4 is used to determine the amount of federal income tax that should be withheld from an employee’s paycheck. It takes into account factors like marital status, number of dependents, additional income, deductions, and any extra withholding amounts the employee wishes to specify.

- Immediate Relevance to Paychecks: The information provided on Form W-4 directly impacts the net amount an employee receives in their regular paychecks. It’s the form that bridges an employee’s earnings and the deductions for taxes that are taken out of each paycheck.

- Adjusting Tax Withholding: Understanding how to fill out Form W-4 allows individuals to adjust their tax withholdings to better match their actual tax liability. This is crucial for individuals who want to avoid having too much or too little tax withheld throughout the year.

Click this link to download the 2024 Form W-4 document

Please note that when it comes to federal income tax, there is nothing specific to mention about the state because federal income tax is standardized across the United States. The rates and the way it’s calculated do not change based on the state in which you reside or work.

The Internal Revenue Service (IRS) is the federal agency responsible for tax collection and tax law enforcement across all states, and they use the same rules and tax brackets for all U.S. residents. The details that an individual needs to provide on Form W-4 for the calculation of federal income tax withholdings are consistent for every state. These details include:

- Personal information and filing status

- Multiple jobs or spouse’s employment

- Dependents

- Other income

- Deductions outside the standard deduction

- Any additional amount the employee wishes to withhold

Let’s now review the W-4 Form and how to fill it in together:

Understanding the W-4 Form

Step 1: Enter Personal Information: At the top of Form W-4, you’ll fill in your name, address, Social Security number, and filing status (single, married filing jointly, married filing separately, or head of household).

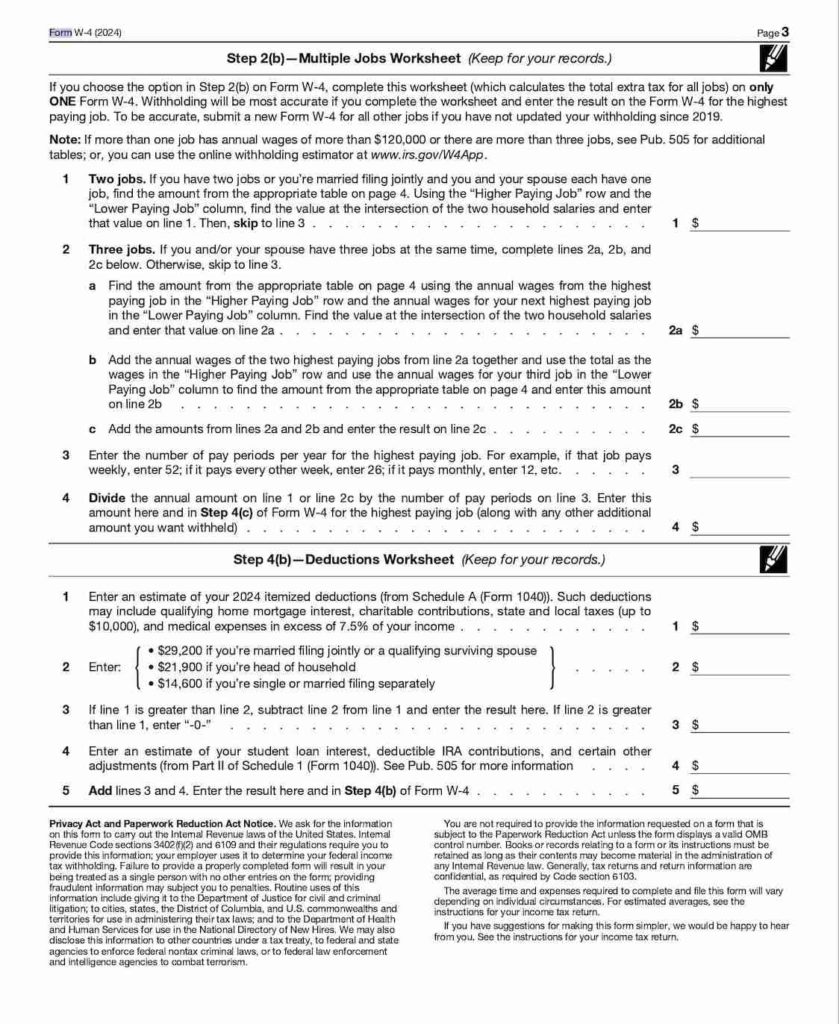

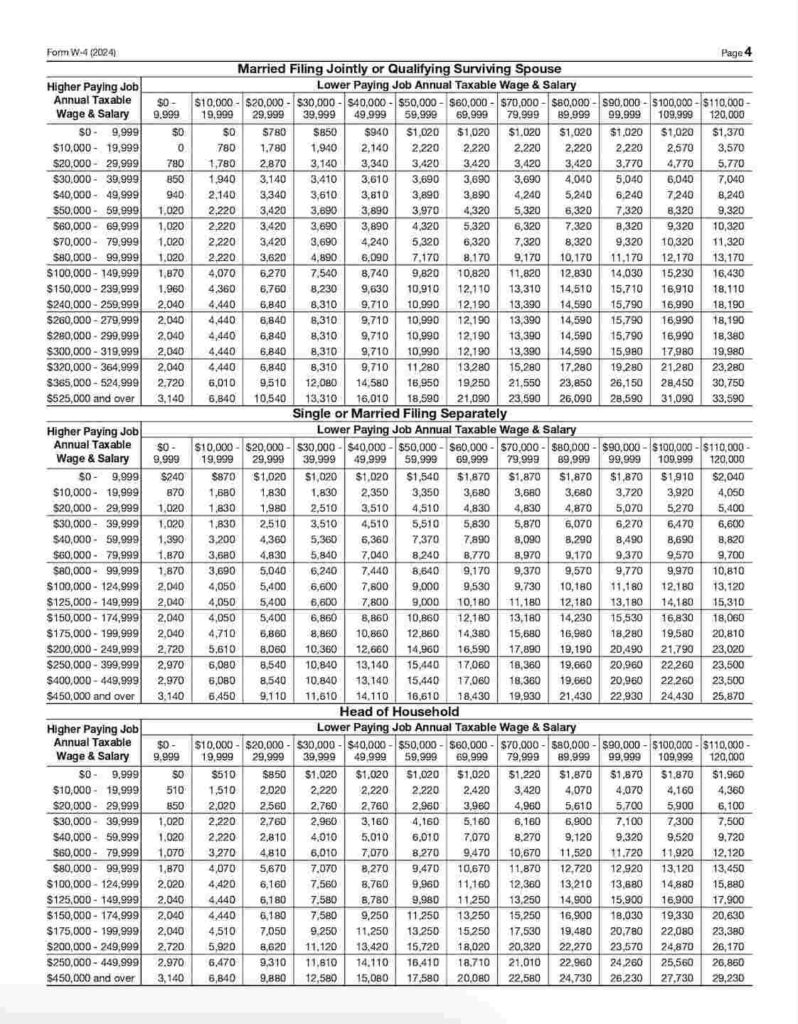

Step 2: Multiple Jobs or Spouse Works: If you have more than one job or you’re married and your spouse works, you have a few options:

- Use the IRS’s online Tax Withholding Estimator for a more precise withholding amount.

- Use the Multiple Jobs Worksheet on page 3 of the W-4 form for a rough estimate.

- If there are only two jobs total, you can check the box in Step 2(c) on each W-4 form.

Step 3: Claim Dependents: If you have dependents, Step 3 allows you to claim child tax credit and credit for other dependents, which can reduce the tax withheld.

Step 4: Other Adjustments:

Step 4(a): If you have other income (like interest, dividends, or retirement income), you can specify an additional amount of tax to withhold.

Step 4(b): If you expect to claim deductions other than the standard deduction, you can reduce your withholding by indicating these deductions here.

Step 4(c): If you want any additional tax withheld from each paycheck, you can specify this amount here.

Sign and Date: Complete the form by signing and dating it before handing it over to your employer.

Step 5: Sign and Date: Complete the form by signing and dating it before handing it over to your employer.

Once you have filled out your form, give the completed Form W-4 to your employer, not to the IRS. Typically, you should submit it to your payroll or human resources department. Keep a copy, and your employer will use the information to update your tax withholding amounts.

Tax Withholding Estimator

If you would like to estimate your federal income tax liability before your employer processes your W-4 and adjusts your withholdings, you can use the following tool:

Click here to estimate your federal income tax

Once you are done with that, please continue to the next step on this article:

Paycheck Calculator: What is My State Income Tax in Colorado?

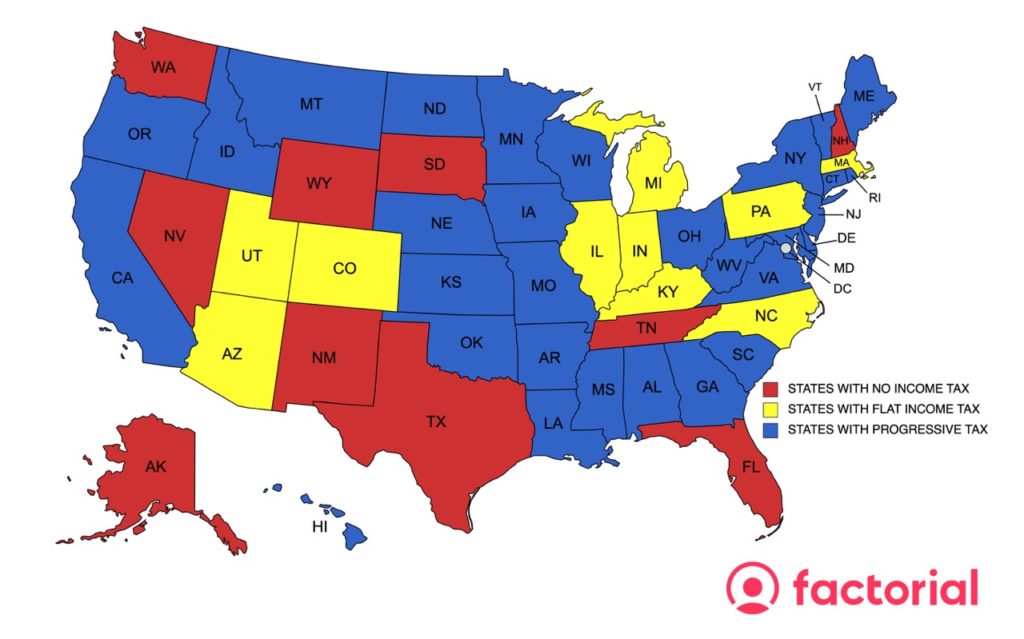

“State Income Tax” refers to the taxes collected by individual states on your income. Unlike federal income taxes, which are consistent across the U.S., state income taxes can vary widely from state to state.

States with no income tax

There are nine states without a state income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. In New Hampshire, dividends and interest are taxed at 5%, and in Washington, capital gains are taxed at 7%.

When you don’t have to pay state income taxes, you might be tempted to pack up and move to Texas, but those states may have higher property taxes, sales taxes, and other fees.

States with flat income tax rates

The states with a flat income tax rate are: Arizona, Colorado, Illinois, Indiana, Kentucky, Massachusetts, Michigan, North Carolina, Pennsylvania, Utah.

There are several states that apply the same tax rate to most income to keep things simple. The definition of “income” varies by state. For example, in New Hampshire, regular income is generally exempt from state taxes, but dividends and interest income are taxed at a flat rate. There are some states that apply their tax rates to taxable income, while others use adjusted gross income.

States with progressive tax structures

There are many states and the District of Columbia that tax income in a similar way to the federal government: They tax higher levels of income at higher rates. Generally speaking, state income tax rates are lower than federal rates. Many are between 1% and 10%. Some even tax just 0% on the first few thousand dollars. Most high-tax states top out around 13%, on top of property taxes, sales taxes, utility taxes, fuel taxes, and whatever the taxpayer has to pay to the federal government.

What is My State Income Tax in Colorado?

For state income taxes, Colorado uses a flat tax system. A flat tax system imposes the same tax rate on everyone, regardless of their income level. Compared to progressive tax systems, where taxes rise with income, this is easy to calculate.

In 2024, Colorado is keeping its individual income tax rate at 4.55%, mirroring the rate in 2023 and 2022. This shows the state has been consistent in its fiscal approach.

To illustrate how this flat tax rate works, let’s consider an example:

Let’s say you’re a Colorado resident and have a taxable income of $60,000. According to Colorado’s flat tax system, you would pay state income tax by applying the uniform tax rate of 4.55% to your entire taxable income in 2024. Your state income tax would be 4.55% of $60,000.

Using this method, residents can estimate their tax liabilities and plan their finances.

Let’s explore your TICA Tax for North Carolina:

Paycheck Calculator: What are My FICA Taxes in Colorado?

FICA taxes are more straightforward, they are federal payroll taxes that fund Social Security and Medicare.

It doesn’t matter which state you’re in — these federal taxes are consistent nationwide because they fund Social Security and Medicare, two programs that are crucial for Americans across the board.

Breaking Down FICA Taxes

As an employee, you pay:

-

Social Security Tax: This tax is assessed at a rate of 6.2% of your gross wages up to a taxable maximum, known as the “Social Security Wage Base.” For the year 2023, this threshold is set at $160,200. This means that once your earnings exceed this limit, you no longer have to pay the Social Security tax for the remainder of the year.

-

Medicare Tax: The Medicare tax rate is 1.45% and is applied to all your wages without a cap. However, there is an Additional Medicare Tax for high earners. If you earn more than $200,000 as a single filer or $250,000 for married couples filing jointly, you’re subject to an additional 0.9% on the amount over these thresholds.

Here you can find the official link to the IRS with the details.

Your employer matches these contributions for a total of 12.4% for Social Security and 2.9% (plus surtax when applicable) for Medicare. If self-employed, you pay both the employee and employer portions.

In conclusion, your FICA tax contributions in Colorado are identical to what they would be in any other state, reflecting the standardized nature of these federal taxes.

Paycheck Calculator: What Voluntary Deductions are Taken from My Paycheck in Colorado?

Voluntary Deductions from your paycheck go directly to specific accounts or entities for various purposes:

The differences between voluntary deductions and mandatory deductions include their nature, choice of participation, and how they’re applied. Mandatory deductions are the ones we’ve covered so far: Federal Income Tax, State Income Tax, FICA Tax.

How to Apply for Voluntary Deductions

- Review Employer Benefits Package: During annual enrollment periods or when you start a job, check out what your employer offers. These plans typically include health insurance, retirement plans, life insurance, and other optional benefits.

- Enrollment Process: Choose the plans that best suit your needs during the open enrollment period. You may need to fill out forms or select options through an online portal.

- Making Changes: During open enrollment, most voluntary deductions can be adjusted or changed, but some, like retirement contributions, can be changed anytime.

- Consult with HR or Benefits Coordinator: The HR department or benefits coordinator can help you with the enrollment process if you have questions.

As an employer, the best way to manage your Payroll process is by centralizing it with a Payroll Management Software.

")

")